Risk-adjusted rate reductions in Asia-Pacific, and varied specialty renewal outcomes, reflect ‘hard market softening' at 1 April

Published

Read time

- Japan risk-adjusted catastrophe excess-of-loss rates-on-line experienced reductions of 10-15%.

- Specialty renewal outcomes were varied:

- Aviation reinsurance rates-on-line were flat, signalling price stability compared to the 3.5% year-on-year reduction observed at 1 January.

- Marine and energy losses in 2024 were well spread with no major impact on programmes.

- Terrorism reinsurance rates-on-line reduced modestly as direct market conditions softened.

- Direct and facultative treaty markets showed further softening although reinsurers displayed greater discipline whilst capacity deployment was focused across towers despite recent loss activity.

London, 1 April 2025 – Howden Re, the reinsurance, capital markets and strategic advisory arm of Howden, the global insurance intermediary group, observed a moderation in Japanese property-catastrophe reinsurance market pricing at 1 April 2025. There were 10-15% risk-adjusted reductions on catastrophe excess-of-loss programmes, whilst global specialty and direct and facultative reinsurance placements varied by class.

Japanese wind and earthquake excess-of-loss pricing adjusts from high base

Reinsurers sought to protect or grow positions in the lead-up to the Japan renewal amidst higher competition and greater supply, whilst cedents successfully leveraged support for harder-to-place programmes. Pricing has eased from a high base, following successive years of market-driven and post-loss hardening, commencing in 2018 and 2019 in the wake of heavy typhoon activity, including Jebi, Hagibis, Trami and Faxai.

The natural catastrophe loss landscape in Japan and the Asia-Pacific region in 2024 was subdued relative to previous years, contributing to moderation at renewals. The most significant losses of the last 18 months have been the Noto earthquake in January 2024, the Taiwan Hualien earthquake in April and Typhoon Yagi in September. Although the California wildfires earlier this quarter impacted reinsurer operating performance, this did not meaningfully constrain supply at 1 April.

Reduced limit was purchased at the lower end of programmes with some cedents seeking additional top-layer limit to address specific risk concerns. Ceding commissions for proportional earthquake cover increased by approximately two percentage points on average, signalling improved terms, whilst per-risk commissions varied by programme performance.

Japan remains an attractive market for reinsurers due to its high volume, relatively uncorrelated risk and deep pool of underwriting expertise backed by experience and exposure data.

“This renewal is, on balance, a welcome reprieve for buyers in Japan and throughout Asia-Pacific on the back of an extended period of significant rate increases,” noted Andy Souter, Head of Asia Pacific, Howden Re International. “With the recent easing in pricing and stable renewals, it’s a good time for cedents to secure more favourable terms and address specific risk concerns.”

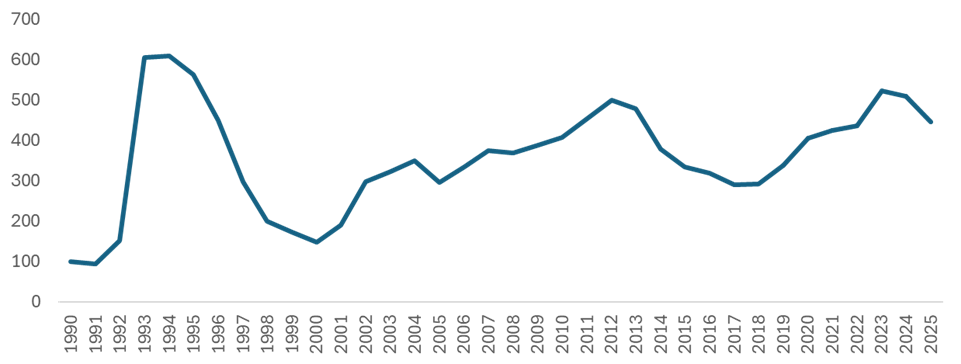

Figure 1: Blended Japan catastrophe excess-of-loss rate-on-line index at 1 April (Source: Nova)

Global specialty in focus

Specialty reinsurance pricing had already eased gradually at the 1 January renewals as capacity returned in the wake of rate hardening following the Russian invasion of Ukraine. Continued uncertainty around war-related losses and macro volatility has nevertheless led to mixed outcomes at 1 April.

Aviation reinsurance risk-adjusted pricing was largely flat at 1 April, representing a slight hardening compared to the 3.5% year-on-year reduction observed at 1 January. Buyers and sellers engaged unusually early, with some programmes essentially placed as soon as the end of last year. Russian leasing losses, included those in some reported claims figures, added complexity to treaty renewals, although these were often categorised as non-segment specific. There is an increasing imbalance between the direct market — with significant over capacity — and the reinsurance market, which is bracing for the potential of impending losses and future hardening.

In a similar vein, additional marine & energy capacity entered the market at 1 January, with healthy growth aspirations from new entrants, adding to the competitive backdrop as established markets also pursued expansion. Whilst there were some downstream losses last year, these were well spread and had little impact on programmes at 1 April. The Baltimore bridge collapse in March 2024 remained in focus as the incident took place within days of last year’s renewal and was therefore largely unaccounted for.

Wildfire exposures were widely discussed, although within marine and energy, the principal focus was specie, where losses have been negligible so far.

Terror reinsurance rates have come down, following softening on the direct side. Consistent event definitions continued to provide stability in an otherwise evolving market. New capacity is simultaneously seeking entry through the MGA channel on both the insurance and reinsurance side, as observed in previous renewal cycles.

The direct & facultative (D&F) market continues to show resilience with strong demand for excess-of-loss capacity despite early 2025 loss activity. Whilst the core open market faces ongoing rate reductions, binder market placements remain firm. Reinsurers demonstrated greater pricing discipline at 1 April compared to 1 January, particularly in response to California wildfire exposures, which were largely retained by cedents. Capacity deployment remained healthy with reinsurers preferring to write across towers rather than chase minimum attachments. Cedents that sought to reduce retentions too far encountered resistance with terms and conditions largely maintained in-line with 1 January levels.

“The April renewal reflected a broad range of outcomes across specialty and D&F lines,” said Chris Medlock, Director, Global Specialty Treaty. “Whilst pricing softened in some areas, reinsurers remained selective and disciplined. Capacity was available but placement success depended on structure, exposure and underlying risk quality.”

Capital flows support capacity for buyers

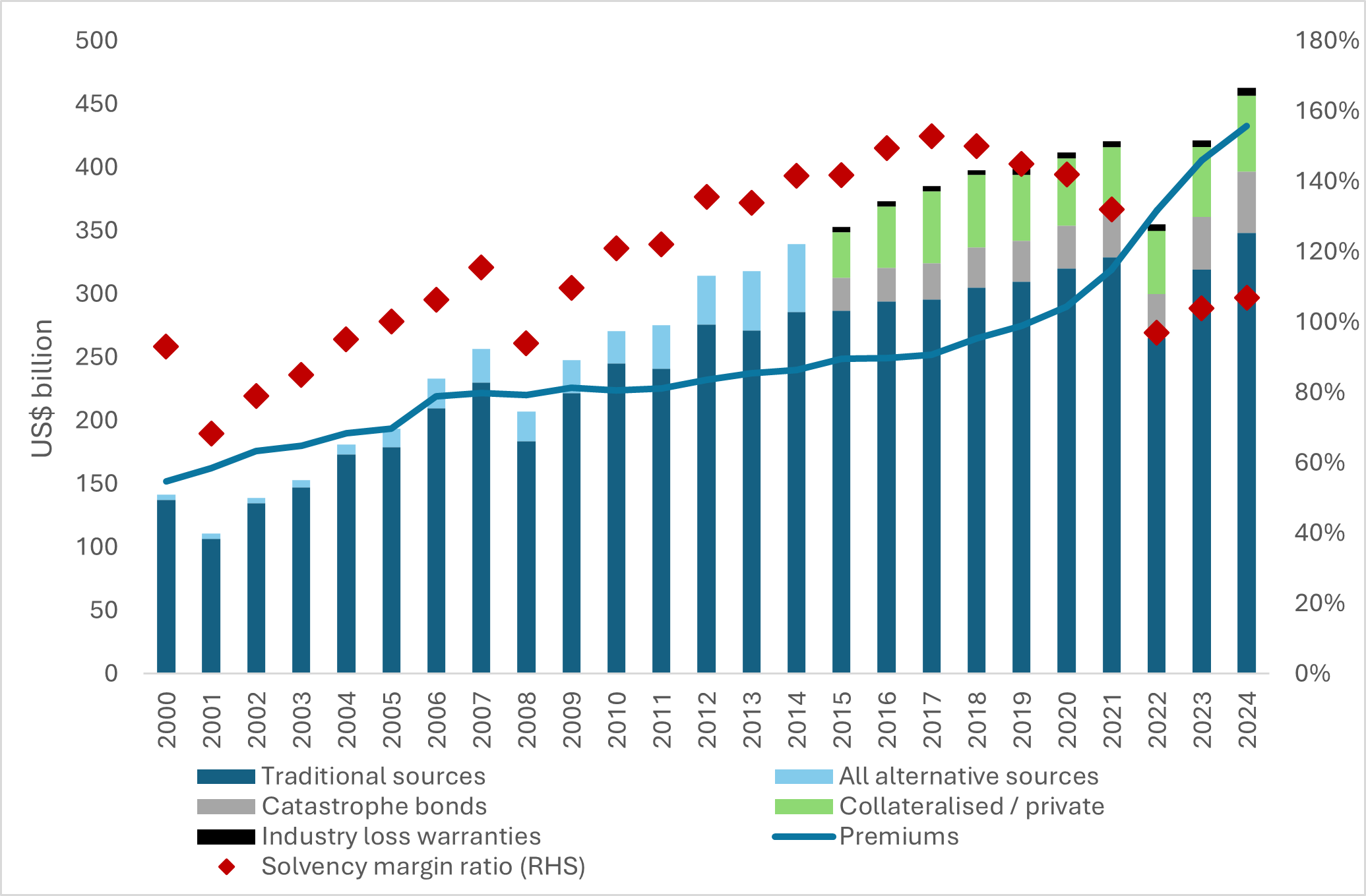

Rising levels of dedicated reinsurance capital and robust ILS market inflows have facilitated pricing moderation in most classes at 1 April. Capital levels now surpass their previous peak following the significant impairment experienced in 2022 and subsequent recovery throughout 2023 and 2024 (Figure 2). This increase has been bolstered by record catastrophe bond issuance, which has continued in earnest during the first quarter of this year. Whilst reinsurers have reported healthy earnings and strong book value growth, it is becoming clear that future gains will increasingly depend on strategic innovation, rather than pricing momentum alone.

“At this stage of the pricing cycle, profitable growth increasingly requires a greater focus on product development, underwriting strategies and capital management,” noted David Flandro, Head of Industry Analysis and Strategic Advisory, Howden Re. “In order to navigate this market phase, comprehensive, integrated capabilities spanning treaty, facultative, MGAs, strategic advisory and capital markets, Howden Re is uniquely positioned to support cedents and reinsurers as they navigate this next critical phase of the cycle.”

Figure 2: Dedicated reinsurance capital and gross premiums 2000–2024