Moderated risk-adjusted property-catastrophe reinsurance pricing reflects shifting market dynamics at 1 June

Published

Read time

- Risk-adjusted property-catastrophe rate-on-line 5% lower on average

- Dedicated sector capital now exceeds 2021 levels

- A notable increase in insurance-linked securities (ILS) market activity with over USD 3 billion of issuance covering Florida perils year-to-date

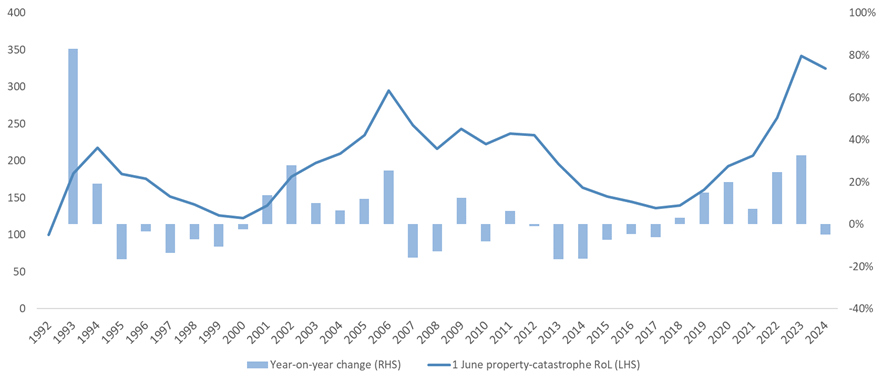

London, 30 May 2024 – After notable rate increases in 2022 and 2023, Howden Re, the reinsurance and strategic advisory arm of Howden, has observed a moderation in the property-catastrophe reinsurance market pricing at 1.6 2024, with average risk-adjusted property-catastrophe reinsurance rates-on-line 5% lower within a typical range of -7.5% to -2.5%.

A period of adjustment

The reinsurance market is experiencing a period of adjustment, due in part to a resurgence in dedicated sector capital, which now exceeds 2021 levels. This recovery, supported by strong ILS inflows, has increased capacity at the top of programmes and led to risk-adjusted rate reductions in higher layers.

Buyers and sellers engaged early in the year, with cedents targeting better terms and conditions to address previous increases in limits and attachments, as well as narrower wordings. Reinsurers exhibited a proactive stance by completing many programmes early, enabling the deployment of increased retrocession capacity as the renewal drew near. This strategic approach enabled some buyers to achieve more favourable terms in what remains a cautious market.

Wade Gulbransen, Howden Re Head of North America, commented, “It is crucial that our clients secure optimal coverage in this rapidly evolving landscape. This means not only finding capacity, but also ensuring it aligns with their risk profiles and financial objectives. Our focus remains on providing innovative thinking alongside dynamic placement strategies to meet these challenges head-on.”

Figure 1: Risk-adjusted property-catastrophe reinsurance index at 1 June

Increased capacity, shifting focus

The ILS market saw a notable increase in activity and competition, with over USD 3 billion of issuance covering Florida perils alone so far this year. Larger Florida carriers have been particularly active in issuing catastrophe bonds, contributing to the increased supply in higher layers. Collateralised retrocession capacity has likewise expanded, with capital providers’ assets under management growing significantly.

Some reinsurers have begun to re-focus on property risks, aiming to grow in peak zones including southwest wind. This shift follows strong performances in 2023, with many reinsurers reporting their best financial results in decades in terms of combined ratio, return on equity, and economic value added. The increased level of ILS interest reflects a broader market trend towards diversified alternative risk transfer mechanisms, offering reinsurers and cedents more options to manage their exposures.

Countervailing factors

Several factors could nevertheless exert short-term rating pressure. Forecasts indicate the potential for a notably active 2024 hurricane season[1]. This follows weakening El Niño conditions and a 60% chance of La Niña developing midseason[2], which typically portends stronger storms. Additionally, Hurricane Ian loss estimates have risen, and there are persistent challenges in lower layers, especially below the 10-year return period. These elements underscore inherent market volatility and the need for strategic resilience.

David Flandro, Head of Industry and Strategic Advisory at Howden Re, added, “The reinsurance market is at a critical juncture. While the recovery of dedicated capital and increased capacity signal a potential softening of rates, the forecasted active hurricane season and other market pressures could counteract these trends. Strategic adaptability and expert guidance are essential in navigating these dynamics.”

Conclusion

Whilst there are signs of downward pressure on property-catastrophe reinsurance rates due to capital recovery and increased market capacity, reinsurers remain vigilant. The anticipated active hurricane season and other market factors could still present significant challenges. Howden Re is committed to closely monitoring these developments and working with clients to navigate the evolving market landscape.

[1] Department of Atmospheric Science, Colorado State University. “Tropical Weather & Climate Research: Forecasting.” Colorado State University, https://tropical.colostate.edu/forecasting.html. Accessed 28 May 2024.

[2] National Weather Service. “El Niño and La Niña.” National Oceanic and Atmospheric Administration, https://www.weather.gov/twc/enso. Accessed 28 May 2024.